Economic Viewpoints: Inflation Came Down in May But Was Still High

Source: U.S. Chamber of Commerce

Author: Curtis Dubay, Chief Economist, US Chamber of Commerce

Retail sales rose 0.3% in May. In April, sales rose 0.4%.

June 16, 2023

Why it matters: Retail sales declined in February and March after a big jump in January. Two months of consecutive growth is encouraging.

But: Consumers’ ability to spend is still likely to decline as the year goes on. Inflation is only now slightly below wage gains and savings are spent down while credit card balances have risen sharply.

By the numbers:

- Sales were up at motor vehicles and parts dealers (1.4%), furniture stores (0.4%), electronics and appliance stores (0.2%), building material and garden supply stores (2.2%), food and beverage stores (0.3%), sporting goods and hobby stores (0.3%), general merchandise stores (0.4%), non-store retailers (mostly online sellers) (0.3%), and food and drinking places (0.4%).

- Sales were down at gas stations (2.6%) and miscellaneous stores (1%).

Looking ahead: A robust job market could put a floor beneath consumer spending and keep it stronger than in previous economic slowdowns.

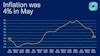

Inflation Came Down in May But Was Still High

June 14, 2023

The Consumer Price Index, the broadest measure of consumer prices, rose 4% annually in May but was down from April, when it was 4.9% and well down from the peak of 9.1% in June 2022.

- On a monthly basis, inflation rose 0.1% from April to May. This is a drop from March to April when prices rose 0.4%.

Why it matters: Despite the progress, inflation remains well above the 2% target and the underlying data is more concerning.

- Core prices, which strip out volatile elements like food and energy, rose 5.3% on an annual basis and 0.4% from April to May.

- The Federal Reserve looks more closely at core prices than the overall inflation number.

Looking ahead: The Fed could still pause interest rate hikes at its meeting this week, but if core prices continue to remain high, it will have to resume rate increases, perhaps as soon as July.

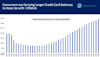

Credit Card Debt Surges in April

June 9, 2023

Consumers are spending up their credit card balances at a sharp rate. In April, they rose 1.1%, and in March they rose 1.2%.

Why it matters: This could have significant repercussions for consumer spending and economic growth.

- The big picture: During Covid, consumers paid down their credit card balances by $127 billion.

- Consumers added $272 billion to their credit card balances since March 2021. Balances are now 13% larger than their pre-Covid peak.

However, income has grown in that period. As a share of income, credit card debt is still below its pre-Covid level and well below its average over the last 20 years.

Looking ahead: Consumers can’t add much more to their card balances, especially with tightening credit standards. Credit will be less able to bridge the gap between inflation and wages (inflation is still rising faster than wages). This could put downward pressure on consumer spending, which would also put downward pressure on economic growth.

339,000 Jobs Created in May

June 7, 2023

The labor market remains hot, making it more challenging for the Federal Reserve in its efforts to tame inflation.

- 339,000 jobs were created, while expectations were for 188,000.

Why it matters: The labor market is the most important data point the Fed looks at when gauging how its policies affect inflation.

Be smart: The labor force grew by 130,000. We are now almost 2.4 million workers above the pre-pandemic participation level.

- But, if we had the same participation rate now as in February 2020, there would be 1.95 million more workers in the labor force.

By the numbers:

- Wages rose 0.3% from April and 4.3% annually from May 2022.

- Education and Health added 97,000 jobs; Professional and Business Services 64,000; Government 56,000; Leisure and Hospitality 48,000; Construction 25,000.

- Industries that lost jobs in May were Information (9,000) and Manufacturing (2,000).

What's next: With another strong jobs report, the Fed is likely to raise rates again when it meets later this month.

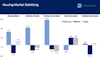

What’s With the Resilient Housing Market?

May 26, 2023

Despite the enormous headwinds from sharply higher mortgage interest rates, the housing market is proving to be resilient after demand fell off steeply when interest rates initially rose.

Why it matters: Demand for homes still exceeds supply, and prices are likely to remain steady as long as this situation continues.

Details:

- Home builders’ optimism is up in recent months.

- Housing starts are rebounding. New permits are down the last two months, but that’s after a 10% jump in February.

- New Home sales were up 4% in the last two months. Existing home sales are down the last two months, but that was after a 14% gain in February. Pending sales were flat in April.

Be smart: Even with higher mortgage rates, there are still more buyers than sellers.

- Buyers are coming back into the market because prices have come down as interest rates have risen.

- Supply is constrained because existing homeowners are hesitant to put their homes on the market, giving up a low-rate mortgage for one with a higher rate.

Looking ahead: While prices will stay below pandemic highs, expect them to remain steady as long as demand outpaces supply.

Business Economists Forecast Modest Growth Through 2024

May 24, 2023

Business economists are lukewarm on the economy. The National Association of Business Economists (NABE) regularly releases a survey of prominent economists where it asks them about their outlooks for the economy. The responses from their most recent survey are interesting:

Economists in “the latest NABE Outlook Survey are divided as to whether a recession in the U.S. is likely in the next year. The median forecast calls for economic growth through 2024 to be modest. Interest rates are expected to decline and inflation is expected to slow in 2024, while job growth is anticipated to moderate, and the unemployment rate to rise.”

Why it matters: The NABE economic outlook is similar to ours at the Chamber. We see a slow economy in 2023 with a 65% chance of a recession this year.

Looking ahead:

- We do not think interest rates are likely to fall in 2024 unless a significant, unforeseen shock happens to the economy.

- On the debt limit, it’s impossible to know how long it would take for a breach of the debt limit to cause a global financial crisis, so it’s best not to test it.

Read more from the US Chamber:

- Economic Data: Comprehensive quantitative snapshots of business sectors and topics to help business and political leaders make informed decisions.

- Workforce Data: Capturing the current state of the U.S. workforce.

- Small Business Index: The MetLife & U.S. Chamber of Commerce Small Business Index is released on a quarterly basis and is compiled from 750 unique online interviews with small business owners and operators each quarter. The Index delivers a comprehensive quantitative snapshot of the small business sector as well as explores small business owners’ perspectives on the latest economic and business trends.

- Middle Market Business Index: The survey panel consists of approximately 1,500 middle market executives and is designed to accurately reflect conditions in the middle market.

About the authors

Curtis Dubay is Chief Economist, Economic Policy Division at the U.S. Chamber of Commerce. He heads the Chamber’s research on the U.S. and global economies.